Mergers and regulations: Two decades of change in banking

PHOTo / Tim Greenway

Bill Ryan, former CEO of TD Banknorth, says Maine is a good market for banks that focus on customer service. He's pictured near his home in Falmouth.

PHOTo / Tim Greenway

Bill Ryan, former CEO of TD Banknorth, says Maine is a good market for banks that focus on customer service. He's pictured near his home in Falmouth.

One thing Bill Ryan learned during his long career in banking is that there is opportunity in every situation — even a major banking crisis.

Ryan came to Maine in 1989 to help turn around Peoples Heritage Bank after the national savings-and-loan crisis, and retired in 2010 as chairman of Banknorth, the largest Maine-based banking holding company.

After becoming CEO of Peoples Heritage, he made more than 30 acquisitions, turning the renamed Banknorth into a $2 billion company. Later, he managed the sale of the company to Toronto-based TD Bank in 2004. It was a deal that, unlike many such mergers, ended up increasing Banknorth's employment in Maine.

In an interview in his Portland office, Ryan says it's a matter of getting the fundamentals right, sizing up the pros and cons of each situation. “You can have a Ph.D in economics, but that's not necessarily going to give you the right answer,” he says.

Ryan started his banking career in Massachusetts, where he was tagged as a rising young executive and attracted the attention of several mentors. One of the first acquisitions he was involved in was a Vermont company named, by coincidence, Banknorth, during the first major wave of banking mergers.

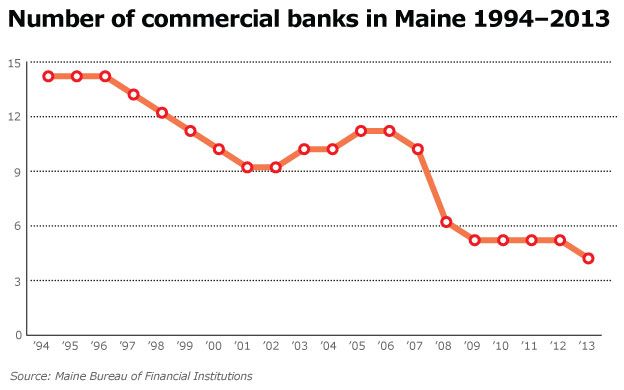

The S&L crisis had hit Maine hard, and deepened the impact of the 1990-91 recession. During the decade 1983-93, 300 New England banks failed, but the survivors, including Banknorth, were well positioned to pick up the pieces.

By contrast, the state's banks were relatively unscathed by the financial crisis of 2008 that shook the world's financial system, though no state escaped the job losses and lingering effects of the ensuing recession.

And the Banknorth sale to TD Bank ended up looking like a stroke of genius. Canadian banks largely escaped the turmoil caused when the largest U.S. banks, with insufficient reserves, had to be rescued by the federal government.

There are many and varied theories about what happened, but Ryan has a simple explanation of why Canadian banks weren't threatened: regulations on mortgage refinancing.

“At the height of the boom, we had customers refinancing their mortgage every month,” he says. “It got to the point no one knew what the real value of these mortgages was. In Canada, you couldn't do that.”

As Peoples Heritage had done after the S&L crisis — buying up weaker banks and recapitalizing them — TD Bank did after the 2008 crisis, starting with New Jersey-based Commerce Bank. TD has acquired banks as far south as North Carolina, and is now a major U.S. player. That in turn has benefited Banknorth, which has increased employment in Maine since the merger, to more than 3,000.

Ryan says reports on the crisis were sometimes overblown. “This is the biggest and most successful financial system in the world,” he says. “There's no way we would have let it fail.” On the other hand, “We did have a complete collapse of the mortgage market,” which continues to ripple through the economy.

“What we had,” he says, “were people who thought they were smarter than everyone else, who believed they understood the real estate market and couldn't fail.”

By the time companies were issuing mortgages with 100% financing, no money down, Ryan knew a collapse was inevitable. “We had these people in my office, telling me all the opportunities we were missing.”

When he asked one banker about the quality of some of the loans being issued, the response was, “We have the best collection agents in the business.”

His response at the time was, “[If] you're depending on collections to make a profit, you're not thinking this through. That was just greed.”

Maine is a good market for banks, Ryan says, once one understands the differences in its economy versus that of other states. “If you're a New England banker, you'd naturally assume Boston is the best place to open a branch.” The average account in Boston is $3,000; in Maine it's $1,000.

“But it will cost you $2 million to build a branch in Boston, while you can do it in Maine for $700,000,” he says. The Maine branch will be profitable after three years; it will take five years in Boston.

There's also a less turnover in accounts, Ryan says. “Once Maine people are satisfied with a bank, they'll stay indefinitely. In Boston, accounts turn over every year.”

The mortgage crisis changed how a bank's success is measured, Ryan says. Pre-crisis, banks expected gross earnings of 10% and a 1% return on assets. “A lot of banks earn less than 1% today,” he says. “It's the new paradigm.”

He doesn't expect changes in banking to slow down, either. Already, banks are rethinking their bricks-and-mortar investments; many are closing branches as customers shift to mobile banking.

Banknorth, he says, would not have been able to afford the large investments needed to provide secure banking over electronic channels, but TD Bank can.

Yet he says there's opportunity for smaller institutions, not only for the former Maine thrifts that became regional banks, but for larger credit unions, which have grown significantly since the 1990s. “In the end, it's always about how well you can serve your customers and meet their needs,” he says.

Ryan has a prediction about the ongoing battle between banks and credit unions over the latter's exemption from state taxes, which he describes as “a significant competitive advantage.” Ultimately, he says, Maine will tax at least the larger credit unions — not so much to level the playing field, as bankers see it, but because the state would like the windfall.

“Legislators won't see a good reason to pass up the tax revenue,” he says.

As for the future security of the banking system, Ryan takes a skeptical view. Banking crises recur even though each time “we say it will be the last one,” he says. Regulators need to do their jobs, re-examine risks, and step in before things get out of hand — something he admits is easier said than done. Changing rules to allow banks “to go to the government for help” before they fail could be effective. “Unfortunately, our approach now is to let them fail, and then bail them out,” he says.

The multi-billion-dollar fines imposed on large U.S. banks will no doubt have some impact. “That's a lot of money even for banks of this size,” he says. It would have been more effective, Ryan says, if the Justice Department brought charges that sent bankers to jail, as happened following the S&L crisis.

“It's one thing to pay a fine, even in the billions, and quite another to see another banker go to jail,” he says. “That's something these guys always take seriously.”

Ryan retired in 2010, but he's not quite done with banking. He recently agreed to serve as chairman for Berkshire Hills Bancorp in Massachusetts, though it's a part-time commitment. He splits time between Falmouth and Florida, and has served on many boards, including those of Maine colleges and universities such as Colby, Thomas and the University of New England.

If he has some parting advice on how to tell a good deal from bad one, it is this: “Never do business with people who can talk faster than you can think.”

Read more

'He wheeled and dealed': An interview with Mainebiz founder Jon Whitney

Maine's mix of colleges and universities have created an 'education hub'

Health care crossroads: Rising costs coupled with need to be affordable

Oil, propane expected to remain stalwarts as Mainers try new energy sources

Growth engine: Faster broadband seen as essential for Maine's economy

Forest products industry puts $8 billion into Maine's economy

Know your farmer: Locally sourced food trend buoys Maine farms

An industry, changed but still viable: One man's tale of Maine manufacturing

Groundfishing aground? The rise and fall of Maine's offshore fishing industry

Decades of tide changes: Investments help Bath Iron Works maintain its shipbuilding prowess

Reflecting on 20 years: Other 20-year-old companies look back

'He wheeled and dealed': An interview with Mainebiz founder Jon Whitney

Health care crossroads: Rising costs coupled with need to be affordable

Oil, propane expected to remain stalwarts as Mainers try new energy sources

Growth engine: Faster broadband seen as essential for Maine's economy

Forest products industry puts $8 billion into Maine's economy

Know your farmer: Locally sourced food trend buoys Maine farms

An industry, changed but still viable: One man's tale of Maine manufacturing

Groundfishing aground? The rise and fall of Maine's offshore fishing industry

Decades of tide changes: Investments help Bath Iron Works maintain its shipbuilding prowess

Reflecting on 20 years: Other 20-year-old companies look back

Mainebiz presents a 20-year retrospective of doing business in Maine

Most Recent

Most Recent

Comments