Unum's on a fast-growth trajectory

Photo / Tim Greenway

Michael Q. Simonds, president and CEO of Unum US, at the Portland office. Unum Group, which last year had revenue of $10.7 billion, is based in Chattanooga, Tenn. It has 10,000 employees, including 2,800 in Maine.

Photo / Tim Greenway

Michael Q. Simonds, president and CEO of Unum US, at the Portland office. Unum Group, which last year had revenue of $10.7 billion, is based in Chattanooga, Tenn. It has 10,000 employees, including 2,800 in Maine.

Photo / Tim Greenway

Chuck Piacentini, vice president of state legislative affairs at Unum, in the insurer’s Portland offices.

Photo / Tim Greenway

Chuck Piacentini, vice president of state legislative affairs at Unum, in the insurer’s Portland offices.

The cluster of a least half a dozen disability insurers around Portland may be one of the state's better kept secrets, but Unum US, which triggered the trend, is poised to break that silence with the recent acquisition of dental and vision products, plans for additional supplemental insurance and exponential growth that boosted aggregate sales by more than $600 million over the past five years.

“The merger [with Starmount Life Insurance Co. of Baton Rouge, La.] was about our growth, and they had expertise and products,” says Michael Simonds, president and CEO of Unum US, who worked his way up to head the company after starting as a temporary administrative assistant in 1994. “For employers, dental and vision coverage are in high demand.”

Unum US, the third-largest employer in Portland, has 190,000 clients across the United States. Starmount's current $180 million in revenue is expected to grow to $500 million over the next five years with the companies' merger, Simonds says.

Unum US is the primary business of Unum Group (NYSE: UNM), a $10.7 billion corporation based in Chattanooga, Tenn. The largest contingent of Unum Group's 10,000 employees, some 2,800, is in Maine. Unum US insurance products include disability, life accident, critical illness, dental and vision for the workplace. It does not sell health or retirement insurance.

Unum Group bought H&J Capital LLC, the parent of Starmount, in a $127 million deal plus net assets that closed last Aug. 1. The deal is expected to be neutral to accretive to Unum's earnings per share in 2017, according to Unum.

Unum Group is a darling on Wall Street, and as a whole delivered favorable operating results across most of its insurance entities in the past few years, according to a Jan. 18 Zacks Equity Research report posted on Yahoofinance.com. Zacks also cited conservative pricing as contributing to profitability over a considerable time.

The group's shares gained nearly 56% in the last year, significantly outperforming Zacks Accident & Health industry's growth of about 32%. Zacks expects the upward momentum to continue on the back of buying Starmount, which can help Unum capitalize on growth in the dental market, part of its strategy to focus more on the employee benefits business.

As of Jan. 1, Starmount's products are being sold now as Unum Vision nationwide and as Unum Dental in the South and Midwest, with more markets to be added by 2018. Starmount has 230 employees. Starmount will continue to be run out of Baton Rouge, Simonds says, but sales and client management will be in local Unum offices in areas around the country including Boston, San Francisco and Chicago. Unum also owns Colonial Life in Columbia, S.C., and some products will still be sold under that brand.

Origins of a marriage

Starmount approached Unum about the partnership after it saw a press release about a small dental business Unum bought in the United Kingdom, Simonds says, adding that about 10% of Unum's business is in the United Kingdom, 90% in the United States and less than 1% in Maine.

“We had looked outside before [for some services] but it would take a lot of capital and time to grow, so we were looking for an entity to become part of,” says Deborah Sternberg, who will remain president of Starmount. “Unum has the capital and distribution. The cultures of Unum and Starmount are similar even though the companies are different in size.” She expects the merger to allow Starmount to double its employee base over the next five years.

“This is a huge opportunity for Unum and its clients as we can be a single provider for additional benefits to its disability and life insurance,” she adds. “Dental is the second-most popular benefit to employees next to medical. A suite of rich benefits is important whether or not the employer contributes.”

Unum estimates that a vision plan for an employee in the workforce could range from $10-$12 per month and a dental plan from $35-$45 per month, depending on factors such as the number of employees covered in the workforce, dependents on the plan, the type of plan and geographic location of the services.

Group disability is less than $25 monthly per person for just the worker, and it replaces about 66% of their income, says Charles Piacentini, vice president of state legislative and government affairs at Unum. Currently, about 30% of non-farm working Americans have access to or sign up for short- and long-term disability.

“Employees underestimate their risk exposure due to sickness or accident, even for the short term,” Piacentini says. He cites a Charles River Associates study commissioned by Unum that shows most employees can't withstand even three months of disability without insurance. And only half of U.S. workers say they could come up with $2,000, which is a typical copay, if something unexpected arose within the next month, according to Unum.

“Workers compensation covers less than 10% and it's only for things that happened in the workplace,” he adds. “The average time to get covered by Social Security disability is 12 months, and the average coverage is $1,200 per month.” Unum's insurance covers the employee wherever the disability happened, which the company says is important with a more distributed workforce and people working at home.

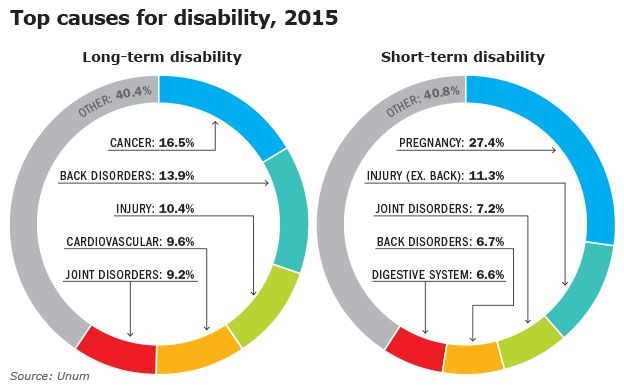

The most common long-term disabilities are cancer and back disorders, while common short-term disabilities are pregnancy and non-back injuries.

Simonds says one in four workers will be out of work on disability for six months or more from the time they enter the workforce until age 65.

“American's aren't as healthy as they used to be,” he adds. “And disability is such an inexpensive coverage.”

Filling the gaps

Piacentini says that while disability is Unum's largest business and the company is the largest disability carrier in the country, other companies grew disability practices in greater Portland including Prudential, Sun Life, Disability RMS and Aetna.

“There's a trained workforce here,” he says. That's good news for Simonds, who plans to hire half a dozen or so underwriters over the next few years as Unum expands its new dental and vision products and adds new or improved insurances.

“More employers are offering health insurance with higher deductibles, so we can help with supplemental insurance,” says Simonds, who estimates about 20% of employees sign up for such insurance as it helps them deal with health care gaps.

“About 60%-65% of Americans struggle to come up with $1,000 in an emergency, so if your health care deductible is $1,000 and you miss work or have child care expenses this can help,” Simonds says. “Supplemental insurance is one of the fastest growing parts of insurance.”

He says Unum is second to Aflac Inc. of Columbus, Ga., in offering supplemental insurance in the United States.

Unum also is adding technology to handle changing workforce trends, such as remote work. “We've made big investments in using the web or mobile technology to reach the distributed workforce rather than having them come into an office and meet in the cafeteria to sign up for benefits,” Simonds says.

Thinking longer term, he'd like to consider adding offerings to help employees with paid medical leaves and even further into the future, pet insurance.

Tapping legal changes

A new state law allows employers to take a $30 tax credit for each new employee signing up for either a qualified short-term or long-term disability plan as of Jan. 1. It excludes employees who were previously covered.

Piacentini was among those lobbying for the new law along with other insurers. While the chances of becoming disabled over one's career are at least one in four workers, and the copays or other expenses can easily eat through savings for employees without insurance, Piacentini says there's a high cost to companies as well.

“Most employers have difficulty if a skilled employee loses their ability to work,” he says. “Private disability will work with the employer to get those individuals back to work, saving the costs to find, recruit, train and hire people to replace the person.”

Unum and other disability providers that have been trying to get out their message about the probability and cost of being disabled say the tax credit is an incentive to get more employees and employers on board.

“The tax credit now encourages more plans to be offered in the workplace,” he says.

More employees signing up also decreases the insurance premium for the entire group. He says the biggest opportunity for insurers now is small- to medium-sized companies, as the largest 5%-10% of companies already participate.

Piacentini says there are safeguards in the new bill that set floors to benefit levels for plans to qualify: 50% of income per month replacement longer term and $200 per week short term.

“We've seen interest from brokers since Jan. 1,” he says. “And accountants tell us the tax credit impact [of $30] is pretty significant. It is 10% of the annual premium cost. That won't be the sole reason to offer a plan. But it defrays the cost and opens the door for employers to offer plans.”

Maine is the first state to pass the tax credit law. Piacentini says Unum and other insurers pushed it there because the state is familiar with the disability industry.

In addition, part of the reason $30 was set as the tax credit number is that it resonated with state lawmakers, who realized private disability helps offset the state's welfare system by protecting a worker's income, Piacentini says.

He adds that, theoretically, the financial impact of the tax credit for the 30% of people with disability insurance now would save the state's welfare coffers $4.4 million, but if insurers increase the number of workers with coverage to 49%, the state would save $7.2 million per year on welfare.

“We think those numbers are low,” he says. “We think this will have an impact on the state's welfare savings, which is important to lawmakers and the governor. We'll start to see results when taxes are filed in 2018.”

Mainebiz web partners

Most Recent

Most Recent

Comments