Processing Your Payment

Please do not leave this page until complete. This can take a few moments.

- News

-

Editions

View Digital Editions

Biweekly Issues

- November 03, 2025

- October 20, 2025

- October 6, 2025

- September 22, 2025

- September 8, 2025

- August 25, 2025

- + More

Special Editions

- Lists

- Viewpoints

- Our Events

- Calendar

- Biz Marketplace

Insurance, flood map changes stand to raise premiums

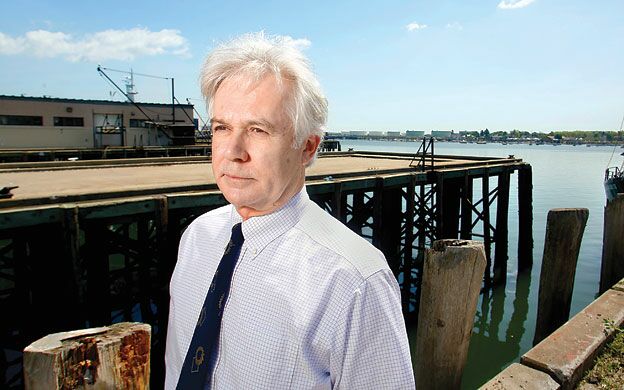

PHOTo / Tim greenway

Bob Gerber, senior engineer and geologist at Ransom Environmental Consulting Inc., along the Portland waterfront

PHOTo / Tim greenway

Bob Gerber, senior engineer and geologist at Ransom Environmental Consulting Inc., along the Portland waterfront

A perfect storm is headed for some coastal Maine properties, but it's not moving in from offshore. It's coming from Washington.

Changes to the federal flood insurance program taking effect this year are set to eliminate flood insurance subsidies gradually for over 3,300 residential and business properties in Maine. Meanwhile, by the end of this year, federal emergency management officials hope to complete revisions of the mostly 20-year-old boundaries dictating which coastal properties in southern and mid-coast Maine are at risk of flooding in a large storm. For existing policyholders with subsidized rates and properties near a floodplain, both changes could drastically boost flood insurance rates unless improvements are made to reduce a property's flood risk.

"It's a shame to see premiums going up, but [the National Flood Insurance Program] is the only game in town," says Wells-based insurance broker Jon Sevigney.

Generally, the changes will move properties to their full risk rates through annual premium increases of up to 25%. Independent of the changes, Sevigney says flood insurance premiums have trended up 8% to 10% over three years, as insurers seek to recover losses incurred from hurricane damage in the last decade.

John DiBiase, the government affairs communications director for the National Association of Realtors, says the reforms stand to affect local real estate markets, but cautions against any broad-based analysis of how rates may change. The NAR supported the reform bill.

"The notion that you can say that if you're right along the coast in Ogunquit, your rates are going up 6% — well, you can't say that because each individual property is different," DiBiase says.

Such rate increase projections remain elusive, but it is clear that York County has the highest number of polices set to lose federal subsidies in Maine, according to a December count by the Federal Emergency Management Agency.

Over one-fourth, or 908, of Maine's 3,319 subsidized policyholders are located in York County. That's nearly double the number in next-highest Cumberland County. Across all Maine towns affected, York County also stands out. Six out of the top 10 Maine towns, ranked by the number of subsidized insurance policies, are in York County.

Of the subsidized policies in York County, 399 will begin seeing higher bills when renewing policies this year; another 272 primary residences in York County newly stand to lose subsidized rates if sold, substantially repaired or if the policy should lapse.

Nationwide, FEMA expects insurance changes rolling out this year will affect 19% of policyholders. Around 81% already pay actuarial rates.

In Maine, however, 36% of flood insurance policies are subsidized. That's because Maine has some of the oldest housing stock in the country, according to Sue Baker, program coordinator of Maine's Floodplain Management Program. Properties built before FEMA's first flood insurance risk maps were accepted — for Maine, the late 1970s and early 1980s — are eligible for subsidized rates.

For one such subsidized policy, Sevigney says rates have already shot up $1,400 to $1,800 in the last three years, a 23% increase.

But how deeply the elimination of subsidized rates will cut remains unclear, Baker says, largely because the state doesn't know the floodplain elevation of all affected properties.

Eventually, nearly all policyholders will pay full freight for their flood risk or make significant structural improvements, like elevating a property or pursuing community-wide mitigation measures.

Those changes are not all bad news, state and federal officials say. They hope the insurance reform will be the first step to keeping the national flood insurance program solvent.

Last summer, when the Biggert-Waters Flood Insurance Reform Act cleared Congress aboard a larger transportation bill, the nation's flood insurance program was over $17 billion in debt to the U.S. Treasury. That figure is expected to approach $25 billion in the wake of Hurricane Sandy.

For real estate markets, DiBiase says, the program's stability trumps the pitfalls of certain properties facing rising premiums.

"Before Biggert-Waters, the flood insurance program was operating under a series of stopgap measures and there was a great deal of uncertainty," DiBiase says. "When that program went offline, it was affecting closures all over the country."

In hurricane-ravaged Louisiana and East Coast communities reeling from Sandy, the one-two combo of new flood maps and phasing out flood insurance subsidies led Louisiana Sen. Mary Landrieu to initiate action to delay parts of Biggert-Waters. Here in Maine, municipal officials, environmental consultants, insurance brokers and engineers are focused on how the state's coast will adapt to the rising dangers, actual and actuarial.

Shorter horizons

As properties in existing flood zones face policy changes, municipal officials in coastal areas expect FEMA's flood map revisions will pose new challenges for communities with millions of dollars in valuable property lining the coast. New flood zone designations could mean higher insurance premiums, development restrictions and decreased property values that could pose a barrier to new development and investment.

Across York and Cumberland counties, Bob Gerber, an engineer and geologist with Ransom Environmental Consulting Inc., is working for 12 municipalities that are trying to get a handle on the potential flood zone changes that were delayed from their May release to later this fall.

Before Biggert-Waters, any properties added to the flood zone could lock in grandfathered rates if they secured flood insurance before the map changes were adopted. But the reforms take that option away, raising the stakes for this next map adjustment.

Contesting those new maps takes more than anecdotal evidence. Gerber says it took 30 years of historical wind speed data in Cumberland County for FEMA to change its parameters for the hypothetical storm that determines flood map boundaries. The agency requires a minimum of 20 years of data to challenge its methods.

When FEMA issued its first round of draft maps for southern Maine, most of Portland's waterfront Commercial Street, which Gerber's office window looks out upon, was identified as facing 3-foot waves in a severe storm, a change that would have put new building restrictions on properties there.

Gerber's analysis of historical wind data and modeling of how Casco Bay's islands dissipate open ocean waves won a more detailed revision of the city's flood zone, sparing all but some pier-end properties from higher flood zone designations.

Similar historical data was not available for York County, so a consistent one-hour, 71 mph wind remains a component in the region's 100-year, or 1%, storm. That rare storm is a combination of extreme winds, storm surge elevation and high waves.

From the new maps, local officials expect big changes in areas like Goose Rocks in Kennebunkport and the expansive marsh behind Wells Beach.

Werner Gilliam, Kennebunkport's town planner, says while it remains unclear just how the maps will turn out after going from preliminary drafts through local review and possible appeals, the work maps he saw earlier this year would "clearly change the building character of these developed areas."

"I see properties going in two directions," Gilliam says. "Either we have folks that have the money buy up multiple properties and build bigger homes, or maybe we'll see a drop in the property values."

Mike Livingston, town engineer for Wells, says he's expecting residents on the easterly side of the town's marsh — where he says deep water and high winds can combine to create intertidal waves — will see increased flood risks identified in the new maps. While final, digital versions of FEMA's latest maps will be required to overlay the proposed flood zones with existing property valuations, Livingston says it's clear that many of Maine's waterfront communities, like Wells, have a significant portion of property taxes coming from coastal properties and, therefore, a stake in the new maps.

Separately, Wells has the highest number of flood insurance policies set to lose subsidies, at 207, of any town in Maine.

But Baker, with the state's floodplain program, says the flood risk changes from the new maps may end up a mixed bag. That's because along with storm data updated since the early 1980s, the new maps will include a greater level of topographical detail, showing elevations at 2-foot increments rather than the 10-foot increments of the current maps.

"The net gain or loss is tough to predict," Baker says. "It will go both ways."

David Mendelsohn, a FEMA community coordination officer based in Boston, says he hopes new coastal maps will be finalized by January and then go for local approval. Once FEMA approves its final maps to send out, a municipality has six months to approve them to continue participating in the national flood insurance program.

What's next

Gerber expects this round of FEMA map updates will be the last for which coastal Maine municipalities hire him to contest the agency's findings.

"I fight for them to get the most reasonable flood levels they can," Gerber says, "but they have to realize they can't hold this tide back forever."

FEMA's flood maps take a historical look at weather patterns and risk. While Gerber says those maps can overstate risk, he sees other ways in which the agency's method of historical analysis might miss real risk factors, like sea level rise.

"Nobody wants to really say how high the water will rise in the next 20 years, but there ought to be something that takes that into account," Gerber says. "But nobody's come up with a method that's acceptable to everyone."

On top of that, he says the agency's analysis continues to use outdated precipitation figures that have been in common use by engineers for decades.

For example, new data show a 24-hour storm now drops around 2 inches more rain on the town of Falmouth than it did in previous reckonings.

Over the next 100 years, Gerber expects sea levels along Maine's coast to rise nearly 3 feet. Should that increase meet with harsh storm conditions in coming decades, the consequences for coastal communities could be dire.

"I expect the whole of Wells Beach to disappear in the next 50 years," he says.

Read more

FEMA reassesses Cumberland, York counties flood risk

Flood insurance timeline

The Biggert-Waters Flood Insurance Reform Act will gradually move subsidized flood insurance policies for certain homes built before the first flood maps were issued to fully risk-based premiums:

Jan. 1, 2013

- Non-primary homes begin gradual premium increases until reaching actuarial rates.

- Primary residences sold, significantly repaired, with policy lapses or purchase of a new policy, will begin paying full, actuarial rates.

Oct. 1, 2013

- Businesses, non-residential and severe repetitive loss properties begin the move to actuarial rates.

Jan. 1, 2014

- Flood map updates will begin affecting all premiums, ending "grandfathering" that tethers rates to maps in effect at the time of construction.

Mainebiz web partners

The Giving Guide

The Giving Guide helps nonprofits have the opportunity to showcase and differentiate their organizations so that businesses better understand how they can contribute to a nonprofit’s mission and work.

Learn More

Work for ME

Work for ME is a workforce development tool to help Maine’s employers target Maine’s emerging workforce. Work for ME highlights each industry, its impact on Maine’s economy, the jobs available to entry-level workers, the training and education needed to get a career started.

Learn More

Groundbreaking Maine

Whether you’re a developer, financer, architect, or industry enthusiast, Groundbreaking Maine is crafted to be your go-to source for valuable insights in Maine’s real estate and construction community.

Learn more-

The Giving Guide

The Giving Guide helps nonprofits have the opportunity to showcase and differentiate their organizations so that businesses better understand how they can contribute to a nonprofit’s mission and work.

-

Work for ME

Work for ME is a workforce development tool to help Maine’s employers target Maine’s emerging workforce. Work for ME highlights each industry, its impact on Maine’s economy, the jobs available to entry-level workers, the training and education needed to get a career started.

-

Groundbreaking Maine

Whether you’re a developer, financer, architect, or industry enthusiast, Groundbreaking Maine is crafted to be your go-to source for valuable insights in Maine’s real estate and construction community.

ABOUT

NEW ENGLAND BUSINESS MEDIA SITES

No articles left

Get access now

In order to use this feature, we need some information from you. You can also login or register for a free account.

By clicking submit you are agreeing to our cookie usage and Privacy Policy

Already have an account? Login

Already have an account? Login

Want to create an account? Register

Get access now

In order to use this feature, we need some information from you. You can also login or register for a free account.

By clicking submit you are agreeing to our cookie usage and Privacy Policy

Already have an account? Login

Already have an account? Login

Want to create an account? Register

Comments