Processing Your Payment

Please do not leave this page until complete. This can take a few moments.

- News

-

Editions

View Digital Editions

Biweekly Issues

- November 03, 2025

- October 20, 2025

- October 6, 2025

- September 22, 2025

- September 8, 2025

- August 25, 2025

- + More

Special Editions

- Lists

- Viewpoints

-

Our Events

Event Info

Award Honorees

- Calendar

- Biz Marketplace

Here's what's driving CEI's strategic plan: 'Our economy has to work for everyone'

Photo / Tim Greenway

CEI CEO Betsy Biemann says she'll earmark more money for companies that are growing and retaining jobs.

Photo / Tim Greenway

CEI CEO Betsy Biemann says she'll earmark more money for companies that are growing and retaining jobs.

A year after its visionary founder, CEO and President Ron Phillips stepped down, CEI's new management set a strategic plan to focus the entire organization on quality jobs, a sustainable environment and shared prosperity for all Mainers, and help pave the way for other rural areas to improve across the country.

Phillips' successor, CEO Betsy Biemann, who made her first public statement of CEI's goals at the company's annual meeting March 14, says she, President Keith Bisson and others picked the priorities based on the belief that hard work at a full-time job should yield a decent livelihood.

“Yet eight million Americans today work full time and live in poverty,” she told the annual meeting attendees, who braved a nor'easter to be at the event in Brunswick. “We're going to begin allocating more of our capital to companies that are growing good jobs and sustaining those jobs, and working with companies to help them develop better jobs and put together workforce training solutions.”

Biemann, a former head of the Maine Technology Institute, told Mainebiz that CEI is “talking about the same thing that everyone else in the country is now talking about: that our economy has to work for everyone.”

She added, “We need to be more intentional to make sure that everyone has access to good jobs, that we have both economic growth and economic opportunity.” Biemann oversees the big picture elements of CEI while Bisson focuses on operations.

One recent success she points to is St. Croix Tissue Inc., which added two tissue machines in a $120 million paper mill expansion that has created more than 80 jobs in a town of 1,500 residents.

But Biemann and CEI have their work cut out for them.

For example, a little-known federal funding program that's making a big difference in jobs and business loans to small communities risks a substantial cut under the Trump administration's proposed budget, submitted to Congress on March 16. The U.S. Treasury's Community Development Financial Institutions Fund, or CDFI, gives loans to institutions, including CEI and its subsidiary CEI Capital Management LLC, both in Brunswick, which focus on disadvantaged areas, including rural Maine. Under CDFI, CEI and CCML were granted a total of $913 million in federal New Markets Tax Credits over the past 10 years.

Fast Company magazine writes that the proposed budget would cut CDFI's funds by $210 million, leaving $19 million to run existing programs.

“The president's budget proposes cutting and eliminating many federal programs that are important to people in Maine and across the country, in both urban and rural places,” CEI president Bisson told Mainebiz in an email. “Many of these programs support R&D, economic development, education and investment in our children.”

He adds, “For example, funding from the … CDFI, which the president's budget essentially eliminates, makes it possible for organizations like CEI to provide loans and investments to business owners who are creating good jobs and growing our economy.”

To Biemann, that's like throwing down the gauntlet. “CEI is more important than ever,” she says. “Week in and week out we are financing businesses that aren't likely to get financed from banks and other investors.”

She adds, “When we took a step back last summer and asked what's next and went to chart the rest of our future, we asked fundamental questions about how the world has changed since CEI made its first loan. We asked, how has the economy been changing and how has that affected people in rural economies and people with low income? Is the lack of fast internet connection a barrier to communities today the same as electricity was 100 years ago? What we didn't anticipate was that by the end of the election, all Americans would be asking these same questions. Is the economy working well for everyone?”

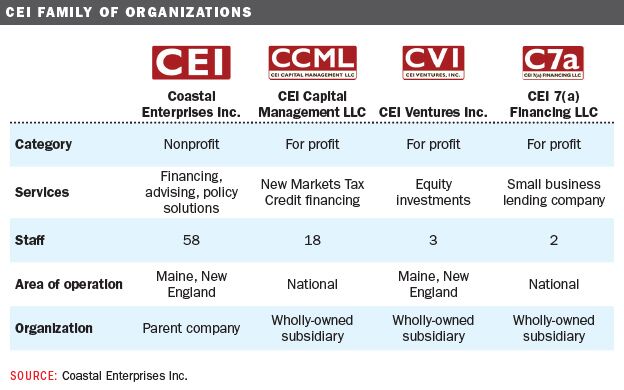

What is CEI?

CEI, with 58 staff in Maine, is a private, nonprofit community development organization that operates in Maine and New England, offering financing, advising and policy solutions. It is one of 4,600 such corporations nationwide, according to community-wealth.org. CEI also has the following teams and programs: Lending and Investing, Maine Small Business Development Centers, a Women's Business Center, StartSmart (to foster immigrant businesses), Workforce Solutions, Natural Resources Sectors, Housing Counseling and Federal/State Policy.

The average size for a CEI micro-, small- and medium-size loan is $116,892 based on data from the past 10 years.

It also has three for-profit subsidiaries. CEI Capital Management LLC, with 18 staff in Maine, operates nationally and focuses on federal New Markets Tax Credit financing. CEI Ventures Inc., with three people in Maine, makes equity investments in Maine and New England (see related story, page 26). And C7(a) Financing LLC is a Small Business Administration lending company with a staff of two in Maine, though it operates nationally.

Rob Wilson, CEO of CEI's newest for-profit subsidiary, CEI C7(a), explains that the three for-profit subsidiaries are owned by CEI but governed by independent boards of directors, the majority of whom are not affiliated with CEI, so they are not CEI board members or CEI employees.

“CEI as the owner sets the overall direction and tone, ensuring that subsidiaries missions and goals are consistent with, and additive to CEI's own mission and goals,” Wilson says.

Biemann told Mainebiz that going forward, she'd like to have a greater alignment across the CRI organizations. For example, a company approaching CEI might be better off getting a microloan, while another might need venture capital or a New Markets Tax Credit. And while all of CEI's operations are known for investing in companies open to hiring low-income workers and to improving their sustainability practices, they're not only focused on rural development.

“CEI broadly finances rural companies, but also those in Portland and Lewiston,” Biemann says.

New Markets Tax Credit

CEI Capital Management, known within CEI as CCML, deploys capital under the U.S. Treasury's New Markets Tax Credit Program and in turn increases opportunities for businesses in rural, low-income communities.

“NMTC was envisioned by Ron and others in the 1980s to leverage more private capital into companies,” says Charles Spies III, CEO of CCML. “We did our first NMTC projects in 2004.” To date, CCML has raised and placed more than $783 million of NMTCs into 82 projects nationwide.

“NMTC give businesses an opportunity to work on a national basis so they can compete for large awards,” he says.

On a $20 million loan, 20% of the loan is a tax credit that a company doesn't have to repay, while 70-80% is paid back to a commercial bank. CCML's involvement helps offset the risk of a loan for which a company might otherwise not qualify.

CCML makes its money in a front-end fee of 3% to 5% depending on the size of the deal to cover the legal and accounting transaction costs along with CCML's fee load, Spies says. So far, only three of CCML's 82 projects went into default.

The federal Community Renewal Tax Relief Act of 2000 authorized NMTCs as part of a bipartisan effort to stimulate investment and economic growth in low-income urban and rural communities that couldn't otherwise quality for loans from banks and traditional funding institutions. It expires on Dec. 31, 2019, though an extension act introduced this year would extend the credits indefinitely, according to the NMTC Coalition. It is unclear what will happen with NMTCs, as they are administered by the CDFI Fund up for big cuts under the Trump budget proposal.

To date, they have been a key part of CEI and CCML financing. St. Croix Tissue benefited from the NMTC program, which Spies says typically best fits such large equipment purchases as they also must stay in place for seven years.

A new subsidiary

CEI's C7(a) CEO Rob Wilson says the new subsidiary gives businesses without enough collateral, that cannot show three years of profit or are otherwise risky to a traditional bank a way to get a loan.

“We have a small business lending license from the SBA,” says Wilson, adding there are 14 such licenses for organizations like CEI. Banks typically participate in the SBA program — about 3,000 Wilson says — which takes some of the risk out of lending to companies the banks wouldn't consider ideal candidates.

“If we make a $1 million loan the SBA will guarantee $750,000 of it, so we bear the risk on the unguaranteed part,” Wilson said. “We are the lender. The borrower pays the SBA fee up front, so they will pay a 3% fee on 75% of the guarantee. We pay half of 1% on the outstanding loan balance. Those fees cover the losses within the program.”

He says the SBA can only bear losses in the 2-3% range on failed businesses. “We can be 10 times more flexible than a bank in our credit decisions,” Wilson says. His C7(a) lending ranges from $250,000 to $5 million. So far, the new C7(a) business has not closed any loans in Maine.

Wilson says his company's upfront fees are its reimbursement for part of the cost of putting together the loan documents.

“We make money from the spread on our cost of capital and floating rate loans based on the Wall Street Journal prime rate,” he says, adding that a lot of organizations can't fill the gap for $500,000 loans.

While CEI is grappling with market and government forces it hasn't had to tackle since Phillips started it in 1977, there are some things, including its overall mission, that stay the same. And the three goals, Bisson says.

“I've worked with Ron for 12 years and he tells you things in groups of three,” Bisson says. “He went to divinity school.”

Mainebiz web partners

Related Content

The Giving Guide

The Giving Guide helps nonprofits have the opportunity to showcase and differentiate their organizations so that businesses better understand how they can contribute to a nonprofit’s mission and work.

Learn More

Work for ME

Work for ME is a workforce development tool to help Maine’s employers target Maine’s emerging workforce. Work for ME highlights each industry, its impact on Maine’s economy, the jobs available to entry-level workers, the training and education needed to get a career started.

Learn More

Groundbreaking Maine

Whether you’re a developer, financer, architect, or industry enthusiast, Groundbreaking Maine is crafted to be your go-to source for valuable insights in Maine’s real estate and construction community.

Learn more-

The Giving Guide

The Giving Guide helps nonprofits have the opportunity to showcase and differentiate their organizations so that businesses better understand how they can contribute to a nonprofit’s mission and work.

-

Work for ME

Work for ME is a workforce development tool to help Maine’s employers target Maine’s emerging workforce. Work for ME highlights each industry, its impact on Maine’s economy, the jobs available to entry-level workers, the training and education needed to get a career started.

-

Groundbreaking Maine

Whether you’re a developer, financer, architect, or industry enthusiast, Groundbreaking Maine is crafted to be your go-to source for valuable insights in Maine’s real estate and construction community.

ABOUT

NEW ENGLAND BUSINESS MEDIA SITES

No articles left

Get access now

In order to use this feature, we need some information from you. You can also login or register for a free account.

By clicking submit you are agreeing to our cookie usage and Privacy Policy

Already have an account? Login

Already have an account? Login

Want to create an account? Register

Get access now

In order to use this feature, we need some information from you. You can also login or register for a free account.

By clicking submit you are agreeing to our cookie usage and Privacy Policy

Already have an account? Login

Already have an account? Login

Want to create an account? Register

Comments