Community development institutions step in where traditional lenders are reluctant to go

Photo / Tim Greenway

Linda Engelhardt and David Kelso (center), owners of Wicked Water Graphics in South Paris, with their financing partner, Glen Holmes, president of Community Concepts Finance Corp. Wicked Water does hydrographic printing, immersing items in a giant tank to adhere graphics and provide a 3D printing effect.

Photo / Tim Greenway

Linda Engelhardt and David Kelso (center), owners of Wicked Water Graphics in South Paris, with their financing partner, Glen Holmes, president of Community Concepts Finance Corp. Wicked Water does hydrographic printing, immersing items in a giant tank to adhere graphics and provide a 3D printing effect.

Photo / Tim Greenway

Linda Engelhardt and David Kelso (center), owners of Wicked Water Graphics in South Paris, with their financing partner, Glen Holmes, president of Community Concepts Finance Corp. The community development financing institution works with a range of small businesses, including ones that might not qualify for a conventional bank loan.

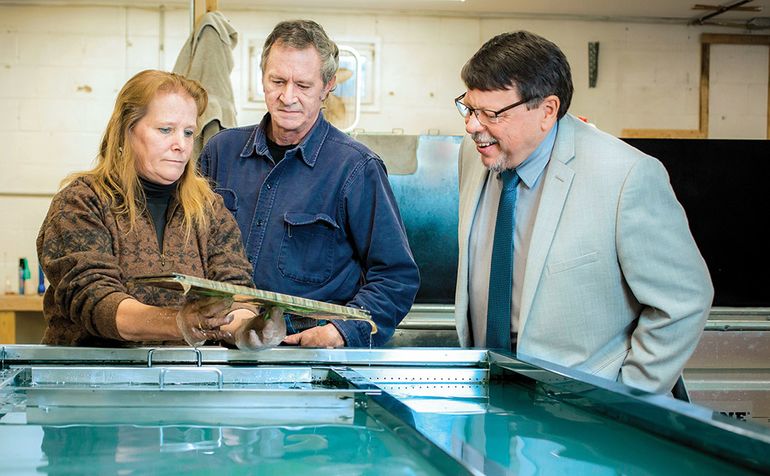

Photo / Tim Greenway

Linda Engelhardt and David Kelso (center), owners of Wicked Water Graphics in South Paris, with their financing partner, Glen Holmes, president of Community Concepts Finance Corp. The community development financing institution works with a range of small businesses, including ones that might not qualify for a conventional bank loan.

In 2017, David Kelso and Linda Engelhardt entered their Madawaska printing business, Wicked Water Graphics, into a fish-and-game expo.

They received great interest in their printing capability on objects like furniture and vehicles. The region's market was bigger than Aroostook County's, so they decided to move. After identifying a South Paris building to buy, they approached a conventional lender for financing.

“They laughed at me,” says Kelso, who explains his equipment didn't provide sufficient collateral.

He contacted Community Concepts Finance Corp., in Lewiston.

“They emailed right back,” says Kelso. “Within two days, one of the finance people there drove to Madawaska to talk with us.”

Community Concepts provided business counseling and a $150,000, five-year loan.

“They really stepped in quickly and stepped up to the plate,” says Kelso.

Personal attention

Community Concepts Finance Corp. is a Community Development Financial Institution, a private sector financial institution that may receive federal funding from the U.S. Treasury.

There are 1,000 such institutions in the country, of which Maine has 11, ranging from Coastal Enterprises Inc. in Brunswick to Eastern Maine Development Corp. in Bangor.

CDFIs like to say they offer personal attention, quick action and flexibility, stepping in where conventional lenders won't.

“The biggest benefit we see is when it comes to economic development,” says Glen Holmes, president of Community Concepts Finance Corp. “If I make a loan to a business, that's the lifeblood of that community. We have communities where there are five businesses and three or four are clients of ours. There wouldn't be a grocery store or a gas station if it weren't for the work we've done.”

The other goal, he says, is to improve the borrower's financial stability in order to transition them to conventional financial institutions.

“We're not competition for the banks,” Holmes says. “We want to get them in shape to use traditional financial institutions.”

Serving the underserved

CDFIs are mission-driven, community-based financial institutions that often make investments — through loans, venture capital, tax credits and other financial services — that make a positive social and economic impact. Their financial products and services are targeted at people and communities underserved by conventional financial institutions, particularly in low-income communities, according to the CDFI Coalition. A key support is the U.S. Department of the Treasury's CDFI Fund, created in 1994 to certify CDFIs and make grants and investments to fund technical assistance and organizational capacity-building.

CDFIs and conventional funding institutions are considered complementary, not competitive. CDFIs often partner with banks to develop innovative loans, investments and financial services, often jointly funding community projects, with CDFIs assuming the more-risky subordinated debt. And CDFIs create a future market for conventional institutions by incubating businesses and people to a level of success acceptable to conventional loan programs.

“One thing I say is, it's an awesome mission and a terrible business strategy, because we're handing off our best clients,” says Chris Linder, CEO of MaineStream Finance, a subsidiary of the nonprofit Penquis. “But if we aren't needed, that's great. We've done our job. In the meantime, we build them up and hand them off. Sometimes it takes two or three or four years, but then they refinance out.”

Strong demand for loans

Keith Bisson, president of Coastal Enterprises Inc. and a board member for the trade association CDFI Coalition, says Maine CDFIs see strong demand for small business lending in sectors like marine and terrestrial food production, but also from early childhood education and childcare facilities. There's a growing trend of loan requests to finance business succession. Maine's food movement and development of clean energy industries likely represent further opportunities, especially for CDFIs' low-income market, Bisson says.

Demand for CDFI services is likely to expand, says Bisson. But, like the larger finance community, CDFIs are vulnerable to political and economic uncertainties.

“Like everyone, we worry about what happens if a recession comes,” he says. “At the same time, CDFIs have been a positive force, as they work with businesses and nonprofits and people and communities in Maine and across the country. We're focused on things that unite us, like creating good jobs in our communities and supporting innovation and services like early childhood education. Those are things that draw people together rather than divide us. So politically speaking, we've had strong support even when there's uncertainty.”

Higher risk

CDFI clients often don't have collateral, a down payment or a good credit history, making them a risky bet for conventional lenders. As such, they pose a higher risk of delinquency. CDFIs generally charge higher interest rates to mitigate risk and also help pay for their more-comprehensive services, which include technical services and business and financial counseling.

At MaineStream Finance, interest rates tend to be higher than a bank's, says Linder.

“We're not a charity. We have to be paid back,” Linder says. “If people don't pay us back today and they see us as a charity, that means we're not helping other clients tomorrow.”

The challenge for the CDFI industry, like the economic development industry in general, is taking reasonable risks, says Will Armitage of the nonprofit Southern Maine Finance.

“We're supposed to take on that level of risk,” Armitage says. “But we have to make sure we're not overexposing ourselves. It's always been a question of, Do we have sufficient funding to fulfill the need that exists?”

Real conversations

The work of CDFIs is characterized by personal attention and a deep understanding of local communities, which also helps to mitigate risk.

Community Concepts, where the default and delinquency rates are less than 3.5%, examines the same things a bank does, like collateral and debt scores.

“But we spend more time with the client, and we're not constrained by regulators,” Holmes says. “We understand that, yes, their credit score is low, but here's why. We want to meet them and understand their dedication and commitment to what they want to build for a company. We have real conversations about that.”

Having more regulatory latitude means the institutions can be more flexible.

“We have the flexibility to be more patient with our financing structure, to work with the borrower,” says Armitage. “If a business experiences a hiccup or slowdown, we can be more patient than the banking industry, because we don't have regulators saying, 'That loan is three months past due.' That flexibility is critical to some of these businesses as they expand or start up.”

Searching for capital

In addition to federal funding, CDFIs attract capital from private and public sources, like corporations, individuals, impact investors and private foundations. They work with conventional financial institutions to channel private investment into distressed communities, either through direct investment in the CDFI or coordination of lending, investment and other services.

Borrowing locally from community banks and credit unions is relatively easy, says Linder. But, just like the small businesses they serve, smaller CDFIs like MaineStream struggle to convince large banks and impact investors outside of Maine to provide capital.

“We're always in search of capital,” Linder says. “Unlike banks and credit unions, we're not deposit-taking. We borrow from banks: It's called wholesale lending. The bank lends to us and we make smaller loans on a retail basis. But sometimes investors or lenders don't want to talk with smaller rural CDFIs, because we don't put up a lot of numbers. We can't say, 'We helped 10,000 people this year.'”

To address the issue, MaineStream, Community Concepts and Four Directions Development Corp. in Orono recently approached larger investors collectively, so they could present larger numbers.

“We've had one success so far,” says Linder. “We'll do that again.”

Education and support

High-distress areas — those with high poverty, high unemployment and low income — particularly benefit from the CDFI model, says Susan Hammond, executive director of Four Directions, a specialized Native American CDFI.

Native communities face unique challenges to economic growth, such as putting up collateral.

“Most lenders need collateral and tribal members don't have the ability to have their property assigned to a non-tribal entity,” Hammond says, explaining that tribal land is often held in trust by the tribe or the Bureau of Indian Affairs, so ownership can't transfer away from the tribe. “We have the flexibility to create loan products and underwriting criteria that address their needs,” she says.

Mainebiz web partners

Most Recent

Most Recent

Comments