Processing Your Payment

Please do not leave this page until complete. This can take a few moments.

- News

-

Editions

View Digital Editions

Biweekly Issues

- December 1, 2025

- Nov. 17, 2025

- November 03, 2025

- October 20, 2025

- October 6, 2025

- September 22, 2025

- + More

Special Editions

- Lists

- Viewpoints

-

Our Events

Event Info

Award Honorees

- Calendar

- Biz Marketplace

Seed capital tax credit program hits its cap

PHOTo / Tim greenway

Josh Davis, co-founder of The Gelato Fiasco and beneficiary of the imperiled Maine Seed Capital Tax Credit Program, in his Portland store

PHOTo / Tim greenway

Josh Davis, co-founder of The Gelato Fiasco and beneficiary of the imperiled Maine Seed Capital Tax Credit Program, in his Portland store

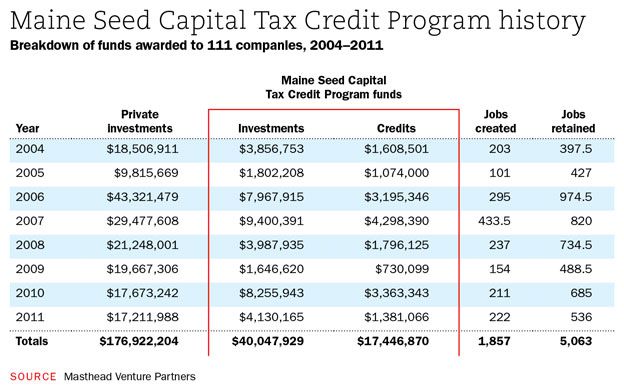

Source: Masthead Venture Partners

Source: Masthead Venture Partners

Josh Davis, co-founder of The Gelato Fiasco, is a big fan of Maine's Seed Capital Tax Credit Program, which his company tapped in 2012 for almost $600,000 in startup capital to expand its wholesale operations into new grocery chains and other retailers throughout the Northeast.

"The Seed Capital Tax Credit was instrumental in helping us expand," says Davis, who, along with his business partner, Bruno Tropeano, was honored at the White House last fall by the national organization Empact as one of the nation's top 100 entrepreneurs under age 30 with revenues over $100,000.

The tax credit program is designed to encourage private equity investments in eligible Maine businesses, directly and through venture capital funds. Prospective investors seeking to use the seed capital tax credits must meet specific eligibility requirements — so must the business. The advantage for prospective investors is that they gain state income tax credits for up to 60% of the cash equity they provide to eligible Maine businesses, spread over four years. The advantage for a startup business, Davis says, is that the tax credit considerably reduces the risk for would-be investors.

"In fact, for a lot of investors, it was the tipping point that helped seal the deal with them," he says. "It made our job a lot easier: Investors know 60% of their investment was protected."

In 2012, the program provided $2.74 million in tax credits to qualifying investors, who invested $4.67 million in 12 Maine companies.

But that venture capital option is no longer available — ironically, due to its success in helping startup manufacturing companies secure scarce venture capital.

The Finance Authority of Maine, which administers the program, served notice in January to Maine businesses seeking venture capital that the tax credit can no longer be allocated because the program reached its $30 million cap, the limit set when the first-in-the-nation program was established by the Legislature in 1989.

"Typically, this is a program I'd be encouraging early startup companies and their investors to consider," says FAME CEO Beth Bordowitz, noting that the shut-off notice went out once her staff realized pending applications exceeded the remaining tax credits allowable under the cap.

Bordowitz says the remedy rests with the Legislature, which could raise the overall $30 million cap or establish a yearly cap, similar to states that have a $5 million or $10 million limit on seed capital tax credits. She says she'd support either proposal.

"It's important for Maine to have a continuum of [venture capital] programs available," she says. "It's been a very successful program. We know a lot of evolving Maine companies that have benefited [from seed capital tax credits being available to their prospective investors]."

District 5 state Sen. Linda Valentino, D-Saco, is sponsoring a bill, LD 743, to establish a $5 million annual cap.

"It's never been a partisan issue, it's always had strong support on both sides of the aisle," says Tim Agnew, a principal with Masthead Venture Partners in Portland, who was FAME's CEO from 1988 to 1999. His company, which also has an office in Cambridge, Mass., specializes in helping entrepreneurs obtain venture capital and develop successful business plans in the early stages of starting their companies.

"In many cases it's the difference between success and failure," he says. "For investors who like to support Maine businesses — particularly small startups that inherently are a risky investment — the tax credit is really what tips the balance and helps them make the decision to invest."

Seeing return on investment

Agnew likens the seed capital tax credit to the third leg of a three-legged financial stool, with R&D spending and the Maine Technology Institute's Innovation Funding Program, along with the Small Enterprise Growth Fund, being the other essential legs of what he characterizes as the state's modest efforts to support early-stage businesses with high-growth potential but high risk of failure.

Undercapitalized businesses, he says, are often unable to get the critical mass of funding and resources to get through that risky early phase — which he describes as the "valley of death" — and move "from concept to product to revenue to growing company." He agrees with Bordowitz that it's essential for Maine to have a continuum of programs making capital available to early-stage businesses, especially because our state lags so far behind New England and U.S. averages in per-capita venture capital investment.

How far behind? According to the National Venture Capital Association, at $11.31 per capita of venture capital investment, Maine spends one-third of Vermont's $33.85, one-ninth of New Hampshire's $96.77, and is barely a blip on the radar compared to Massachusetts's $431.62 per capita VC investment.

"We have a long way to go to attract a level of capital commensurate with the New England region as a whole," Agnew wrote in a seven-page analysis of Maine's Seed Capital Tax Credit Program he put together to help Maine lawmakers understand why restoring the allocation is so critical to the state's ongoing job creation efforts.

In his analysis (see chart, page 22), Agnew found that from 2004 to 2011, FAME issued $17.4 million in seed capital tax credits. That comes to an average of $2.18 million per year. The return on that investment, he says, is demonstrable on several fronts:

- It helped to create 1,856 jobs and retain another 5,000 jobs at businesses receiving the credit during the eight-year period. That translates to an average of 232 new jobs being created each year.

- The tax credits helped leverage $41.0 million in investments from investors using the credit (at a total cost of $17.4 million).

- Businesses attracted $176.9 million in total private investments, for a yearly average of $22.1 million from 2004 to 2011.

"On average, each dollar of seed capital tax credit has attracted nine additional dollars of investment," Agnew says.

Agnew acknowledges that loss of tax revenue represents the downside to the state budget. But that cost, he says, is offset by income and payroll taxes coming into the state budget when new jobs are created by startup businesses using the seed capital program.

Using FAME's job-creation tallies for the eight-year period from 2004 to 2011, Agnew figures there's an average annual cost of $2,282 over four years for each job created as a result of the seed capital tax credit program. Tax revenues for each job and the associated increase in corporate income, he says, average $2,932.

That represents a net gain to the state of $650 per job created, which can continue indefinitely if the business proves to be successful.

"The Legislature has to balance a lot of compelling needs against each other," Agnew says of the fiscal note that would be attached to Valentino's bill. "I strongly believe the seed capital tax credit is an investment of the state with a return to the state … It can do a lot for the state of Maine over a period of time."

Tax credit limbo

Don Gooding, executive director of the Maine Center for Entrepreneurial Development and the vice chairman of the Maine Angels investment group, says he's aware of at least five Maine startup businesses that have used FAME's Seed Capital Tax Credit Program and are likely to use it again.

Another 12 startup companies he's familiar with are likely to look for funding in 2013, and could benefit if the seed capital tax credits become available again.

One of those entrepreneurs is Susan MacKay, co-founder and CEO of Orono-based Cerahelix Inc., a startup that uses nanotechnology to make filtration products that can purify liquids under harsh conditions.

Last year, MacKay says, Cerahelix raised approximately $250,000 in seed financing, which allowed it to apply for 50% matching funds from the National Science Foundation. Of the money raised in Maine, she says, half came from individual investors who took advantage of FAME's seed capital tax credit.

That funding supported the company's efforts in 2012 to develop a prototype and begin to create the infrastructure to support pilot-testing its technology at potential customer sites. The company recently learned it's been awarded three patents for its new technology.

MacKay says her company, founded in 2011, is poised to advance its early-stage product and technology along the development path, where its merits will become better known — and perhaps embraced — in the markets she eventually hopes to capture. It's still a high-risk stage, then, and MacKay says she had planned to tap FAME's seed capital tax credit again to keep forward momentum.

Her elevator pitch? In the next 12 to 18 months she's hoping to have a commercial product ready for sale. And in five years, she's hoping Cerahelix will be a $10 million company with 10 to 15 employees working at a production plant.

"It's not great timing for us," she says of finding the seed capital tax credit option in limbo.

Aside from minimizing the risk for would-be investors, MacKay says another advantage is that its guidelines are straightforward and easy for a startup company or investor to understand. She says other venture capital loan or grant programs can be challenging in terms of the paperwork … which takes away time and energy that startup entrepreneurs could otherwise spend building a foundation for their companies.

"To me, this program has been successful," she says. "It's the kind of money that's nearly impossible to raise [when you're a high-risk early-stage company]."

Investor's perspective

Richard McGoldrick is an angel investor who says he's used FAME's seed capital tax credit for "seven or eight deals" he would not have invested in otherwise — including The Gelato Fiasco and Pika Energy last year.

A former member of FAME's board of directors and the chairman and CEO of Commercial Properties Inc., which has helped develop more than 4 million square feet of commercial space in Maine, McGoldrick considers the seed capital tax credit to be the "most effective economic development tool that's available" for high-risk early-stage companies seeking capital.

"It's using private money directly to promote the development and expansion of small businesses in Maine," he says. "If you look at it with the right eyes, it's an 'investment,' not an 'expense,' [i.e., with respect to the credits' being used by investors to reduce their income tax liability]."

Using The Gelato Fiasco as an example, McGoldrick says the Brunswick-based company was at a critical stage when he decided to tap the tax credit to help with its expansion plans.

"The profit is going to be in the wholesale side of the business," he says. "But you need the branding that comes from the retail presence."

Opening a second Gelato Fiasco store in Portland in early 2012, he says, reinforces the brand in a much larger market than Brunswick — a move affirmed in a big way last fall when the James Beard Foundation's blog recommended the Old Port gelateria as one of five spots to visit in Portland. That kind of positive publicity, in turn, helps The Gelato Fiasco's efforts to get its products into more supermarkets and retail locations throughout the Northeast.

"It would be a shame if this thing went away," McGoldrick says of the tax credit. "It minimizes the risk I wouldn't have taken on with companies that are trying to get off the ground. If you get two or three winners out of 10, you're doing well."

He pauses, then adds: "You can't play the game if you're not in the stadium."

Mainebiz web partners

Related Content

The Giving Guide

The Giving Guide helps nonprofits have the opportunity to showcase and differentiate their organizations so that businesses better understand how they can contribute to a nonprofit’s mission and work.

Learn More

Work for ME

Work for ME is a workforce development tool to help Maine’s employers target Maine’s emerging workforce. Work for ME highlights each industry, its impact on Maine’s economy, the jobs available to entry-level workers, the training and education needed to get a career started.

Learn More

Groundbreaking Maine

Whether you’re a developer, financer, architect, or industry enthusiast, Groundbreaking Maine is crafted to be your go-to source for valuable insights in Maine’s real estate and construction community.

Learn more-

The Giving Guide

The Giving Guide helps nonprofits have the opportunity to showcase and differentiate their organizations so that businesses better understand how they can contribute to a nonprofit’s mission and work.

-

Work for ME

Work for ME is a workforce development tool to help Maine’s employers target Maine’s emerging workforce. Work for ME highlights each industry, its impact on Maine’s economy, the jobs available to entry-level workers, the training and education needed to get a career started.

-

Groundbreaking Maine

Whether you’re a developer, financer, architect, or industry enthusiast, Groundbreaking Maine is crafted to be your go-to source for valuable insights in Maine’s real estate and construction community.

ABOUT

NEW ENGLAND BUSINESS MEDIA SITES

No articles left

Get access now

In order to use this feature, we need some information from you. You can also login or register for a free account.

By clicking submit you are agreeing to our cookie usage and Privacy Policy

Already have an account? Login

Already have an account? Login

Want to create an account? Register

Get access now

In order to use this feature, we need some information from you. You can also login or register for a free account.

By clicking submit you are agreeing to our cookie usage and Privacy Policy

Already have an account? Login

Already have an account? Login

Want to create an account? Register

0 Comments