With more millionaire Mainers, wealth managers are growing quickly, but quietly

PHOTo / Amber Waterman

Brian Bernatchez, president of Golden Pond Wealth Management in Waterville, says many Maine clients embrace a buy-local philosophy when it comes to wealth management services.

PHOTo / Amber Waterman

Brian Bernatchez, president of Golden Pond Wealth Management in Waterville, says many Maine clients embrace a buy-local philosophy when it comes to wealth management services.

Listening to Brian Bernatchez describe his wealth management clients evokes images of Maxwell Smart's “Cone of Silence.” The president of Golden Pond Wealth Management in Waterville says discretion and confidentiality are the hallmarks of advising the wealthy, who, true to their Maine roots, don't like to talk about money.

“I don't acknowledge clients I see in public if I didn't know them socially before. Some won't even come into the office,” he says, adding that you can't judge a book by its cover. “We've had wealthy clients walk in with sawdust in their ears and manure on their boots.”

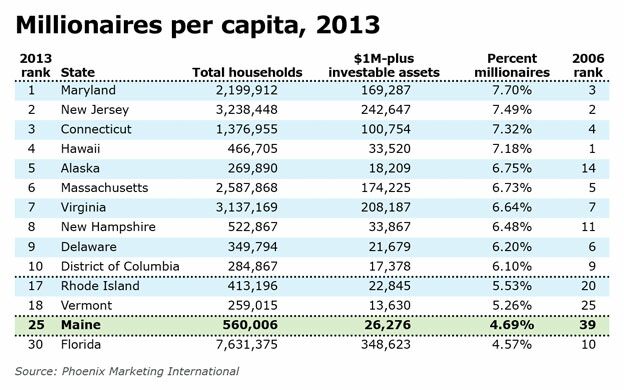

Money can be stressful and emotional, but Maine still is reveling after research firm Phoenix Marketing International ranked the state No. 25 in 2013 in households with more than $1 million in investable assets, typically cash and not including real estate. The state had languished at No. 36 fairly consistently since 2006 in the Rhinebeck, N.Y.-based company's annual report. In 2013, however, 26,276 Maine households, or 4.69% of the state's total, had $1 million or more to invest.

That hasn't escaped the attention of wealth management and financial planning companies in the state, which are largely relying on word of mouth to attract the secretive high net worth customers, some of whom are native Mainers returning to the state, while others are coming from as far away as Hawaii for anonymity. Increasingly, high net worth customers are seeking professional advice from wealth managers, financial planners, financial advisers and other types of investors following the recent recession and the realization that planning premises from the 1990s no longer apply.

Bernatchez says his wealthiest clients aren't actually Maine residents, even though they may live here part of the year. “In most cases, people 'returning' to the state are maintaining their residences elsewhere,” he says, noting that most new clients come in via referrals.

That's because those clients are taking advantage of residency in states with no personal income tax, such as Florida, or those that tax only dividend and interest income, such as New Hampshire (see Bryan Dench's column “Why people with high net worth leave Maine”). A Maine resident is someone who spends more than 183 days total of the tax year in the state.

“This is a front-burner issue,” says Bernatchez of the wealthy “non-resident” Mainers. “It costs the state a lot of money.” He says the state of Maine in the past few years has beefed up its pursuit of people who really are residents and should pay taxes.

David Thompson, author of the Phoenix report, said it's difficult to say precisely why Maine has seen a rise in millionaires, but he figures it is related to the rebound in economic activity in the state in the last few years. “And we've seen at least anecdotal evidence that retirees are looking at other markets than Florida, which has seen a decrease in its wealth population,” he says. Indeed, while Maine climbed the Phoenix wealth chart over the eight years of the study, Florida fell to 30th in 2013 from 10th in 2006. Meanwhile, New Hampshire rose to 8th from 11th.

As expected, the Portland area tops the list of residents with $1 million or more in investable assets, the report found, with 12,410, or 5.7% of the total households in that geography, falling into that asset range. Rockland followed with 4.9%, Augusta-Waterville with 4.5%, Bangor with 4.3%, and Lewiston-Auburn with 3.7%.

But Bernatchez points to other reasons. “We've seen the returning trend in the last five to 10 years,” he says. “The real estate market played a role in it. Typically it's original Mainers or people who have vacationed here. It also has to do with retirement affordability.”

Golden Pond is a fee-based wealth management company, meaning that instead of its managers getting a commission for investment products or services sold to clients, they are on salary. The firm collects a fee based on the amount of assets under management. The company is affiliated with LPL Financial, an independent broker-dealer that provides investments, research, performance reporting and other services to Golden Pond.

The minimum investment for Golden Pond's wealth management clients typically is $500,000, for which the company takes a 1% fee. A separate financial planning service for customers carries an hourly rate.

With $230 million of assets under management, Bernatchez says Golden Pond's clients fall into four general categories: retired educators from Colby, Bates, Bowdoin and the University of Maine; mid- and upper-level management from large manufacturing companies who may have been forced into early retirement; small business owners; and people who still are working. About one-third of the clients are nonprofits.

While definitions and services vary, wealth managers typically handle clients with $500,000 or more to invest and help manage, protect and grow the client's assets, sometimes acting as custodians or trustees. Financial planners typically assess a client's age, income, long-term investment horizon and risk profile and recommend various investments for which they may either charge a fee or commission. Both banks and independent financial companies can do either or both services. Banks are governed by federal and state banking rules and independent financial companies are governed by the Securities and Exchange Commission and state agencies like the Maine Bureau of Securities.

Buying local

Bernatchez says the trend of Mainers to buy local — well known among local “foodies” — also translates to the wealth management sector. Investors wanting more personalized and local management advice than they can get with large Wall Street firms are coming back to Maine.

“Over the last 15 years, there's been a myth that your assets couldn't be managed in Maine, versus Boston or New York. But with those big firms, clients feel like a number,” says James MacLeod, wealth management services director for Bangor Savings Bank, which has $2.5 billion in assets under management, $900 million of which are being held for other clients and $1.6 billion of which are being managed day-to-day.

TD Bank also has seen an influx of high net worth clients, and is expanding its wealth management business accordingly. Michael Iacobucci, regional wealth lender for Northern New England at TD Wealth based in Manchester, N.H., says the company has hired 27 financial services representatives in Maine over the past few years, and now has three portfolio managers in Maine and six officers who are available to clients in the state. He declined to reveal how much assets under management the wealth group has.

“We're continuing to provide a ton of education, training and services,” he says. TD Wealth's clients typically start at $750,000 in investable assets, so the company also has a relationship with TD Ameritrade for other clients. The idea is to give customers a “one bank feel,” he says.

He says the wealth management business takes a goal-driven approach framed toward solutions. “We look at what's the catalyst and have a comprehensive conversation. Are they receptive to an adviser, are they delegators or do-it-yourselfers? Then we can build the relationship model.”

Community banks as a whole benefited greatly from the financial crisis of 2007-2009, with boots on the ground and local customer relationships, says MacLeod of Bangor Savings. That's also true from the late 1990s to early 2000s, when the technology bubble burst, the stock market dove and the 9/11 terrorist attacks occurred. People started to pay attention to who and how and what financial advisers are working for them, he says. “Across the country there was a movement to have a local trusted adviser or a wealth manager rather than a 1-800 number.”

As an indicator of the trend, MacLeod says he has seen Bangor Savings' wealth management business bulge close to sixfold from the $400 million in assets under management when he joined that business in 2004. The bank began its wealth management business and opened a trust department in 1990. He says typical wealth management clients have $500,000 to $2 million, with $100,000 being the minimum to invest. Like Golden Pond, the bank charges a percentage of the investable assets.

Rather than segmenting customers by investable asset size, Bangor Savings groups them by individuals and family, retirement planning and institutional business.

“The larger amounts tend to create different situations that can be complex and have other objectives because of the size, but we don't treat the people any differently,” he says. “To the person with $300,000, that amount of money looks as important to them as someone with $30 million.” He says the bank also takes a team approach, though every account has a portfolio manager by geography and by personality, not by asset size.

The bank also offers financial planning for its wealth management clients for $150 per hour, with a typical plan costing $2,500 to $3,000 to prepare. In particular, baby boomers nearing retirement may be concerned that the investment advice they were given in the early 1990s may no longer be applicable. It was a time, MacLeod says, when some financial planners figured in double-digit investment growth rates, which no longer are realistic.

“Most financial plans fail because the projections and assumptions aren't reasonable,” he says. “There is a double whammy of unrealistic expectations and the stock market decline.” The irony, he says, is that the clients who stuck with a diversified portfolio based on realistic expectations have recovered the losses from the financial crisis, and then some.

Follow the money

Spending is the most important component of whether money lasts, not the market action, contends Daniel Lay, managing director, portfolio manager for H.M. Payson's Institutional Management Group in Portland. The company is an SEC registered investment adviser and Maine trust company.

He says his firm manages clients' long-term assets, considering that if they retire at 60, they need enough money to live for 35-40 years in retirement.

Like Bernatchez, MacLeod and Iacobucci, he's seen an upswing of wealth returning to Maine. “Maine tends to be lower in terms of investable assets [compared to many other states], but it has pockets of wealth,” Lay says. “The concentration of wealth in Northeast Harbor in the summer is higher than anywhere in the world, from July 4 to Labor Day.”

The company has $2.5 billion of assets under management, $500 million to $700 million of which is in trust assets. About $300 million to $400 million is money managed for institutions, nonprofits and municipalities, and the rest are individual assets. The average account size is $1 million, though $500,000 is the minimum to open an account. The fee is 1% for the first $1 million in assets under management, but it decreases as the assets managed increase.

Lay says his greatest source of referrals is existing clients and local professionals. “When times are uncertain, people want certainty,” he says. “We've been around since 1864, with 160 years of investing, through the Civil War, the Great Depression and the World Wars. People want that sort of stability.”

True to the close-to-the vest reputation of New Englanders and their money, he says his company doesn't actively market to the new millionaires coming from New York, Boston and elsewhere who want a low profile. In fact, managers can be dismissed from the firm for mentioning a client without permission.

“It's the way of New England Yankees,” he says, noting that while his clients may not dress like Jed Clampett, the 1960s TV hillbilly millionaire, they also aren't big spenders or big talkers about their money.

“They're frugal. They keep their candle under their basket,” he adds. “This isn't New York.”

Mainebiz web partners

Most Recent

Most Recent

Comments