Updated: April 3, 2023

Checks and balances: Maine banks, believers in safety first, may face bumpy ride if turmoil escalates

Photo / Tim Greenway

Lloyd P. LaFountain III, superintendent of the state’s Bureau of Financial Institutions since May 2005, says that Maine’s banking sector is healthy.

Photo / Tim Greenway

Lloyd P. LaFountain III, superintendent of the state’s Bureau of Financial Institutions since May 2005, says that Maine’s banking sector is healthy.

Bank wobbles and emergency rescues from Silicon Valley to Switzerland turned March into a month of madness for the global financial sector.

Collapses, closures and last-minute rescues — California’s Silvergate and Silicon Valley banks, New York-based Signature Bank, Credit Suisse in Zurich — have rattled financial markets and stoked fears about the durability of smaller, regional banks like the ones found all over Maine.

Maine’s top banking regulator, Lloyd P. LaFountain III at the Bureau of Financial Institutions, warns against overreactions, telling Mainebiz that banks and credit unions in the Pine Tree State are conservative by nature, “so I have every confidence in that sector here in Maine.”

Up and down the state, the consensus is that Maine banks are well-capitalized and diversified, with sufficient buffers to prevent the panicked run that unraveled SVB. But the outlook gets murky if the current turmoil escalates into a wider crisis and sparks a recession.

“We are not California,” says Steven Cunningham, a management and economics professor at Bangor’s Husson University College of Business who has studied the savings-and-loan crisis of the 1980s. “Of course, if people panic and start withdrawing money from Maine banks, it is possible to create a problem.”

Likening what happened at SVB to the Depression-era bank run depicted in Frank Capra’s 1946 film “It’s a Wonderful Life,” Cunningham sees no reason for that to happen in Maine. “It would be totally unwarranted.”

Mark Williams, a finance lecturer at Boston University’s Questrom School of Business, is less optimistic, cautioning that one bad apple — or bank — can spoil the bunch.

“If depositors decide to lose faith in Maine banks, even if they are well-capitalized and the depositor reasoning is unfounded, such banks could be vulnerable,” he says. “Today all banks, even healthy ones, are being questioned by depositors.”

Williams notes that the barrage of credit downgrades of banks including First Republic Bank — after getting a $30 billion infusion from 11 major U.S. banks — has made it harder and costlier for some lenders to raise new debt financing. He’s also concerned over reports of depositors taking their money out of smaller institutions.

Borrowing a phrase made famous by 1992 presidential candidate Ross Perot, he says, “The new giant sucking sound is depositors leaving smaller, regional institutions and going to the bigger banks. That’s a destructive force that should be quelled.”

His recommendation to smaller banks is to market the fact that “they are well-run, safe and sound, and don’t practice excessive risk-taking with depositor funds.”

Williams also suggests prominently displaying the Federal Deposit Insurance Corp. sticker on their websites and front doors.

Where SVB went wrong

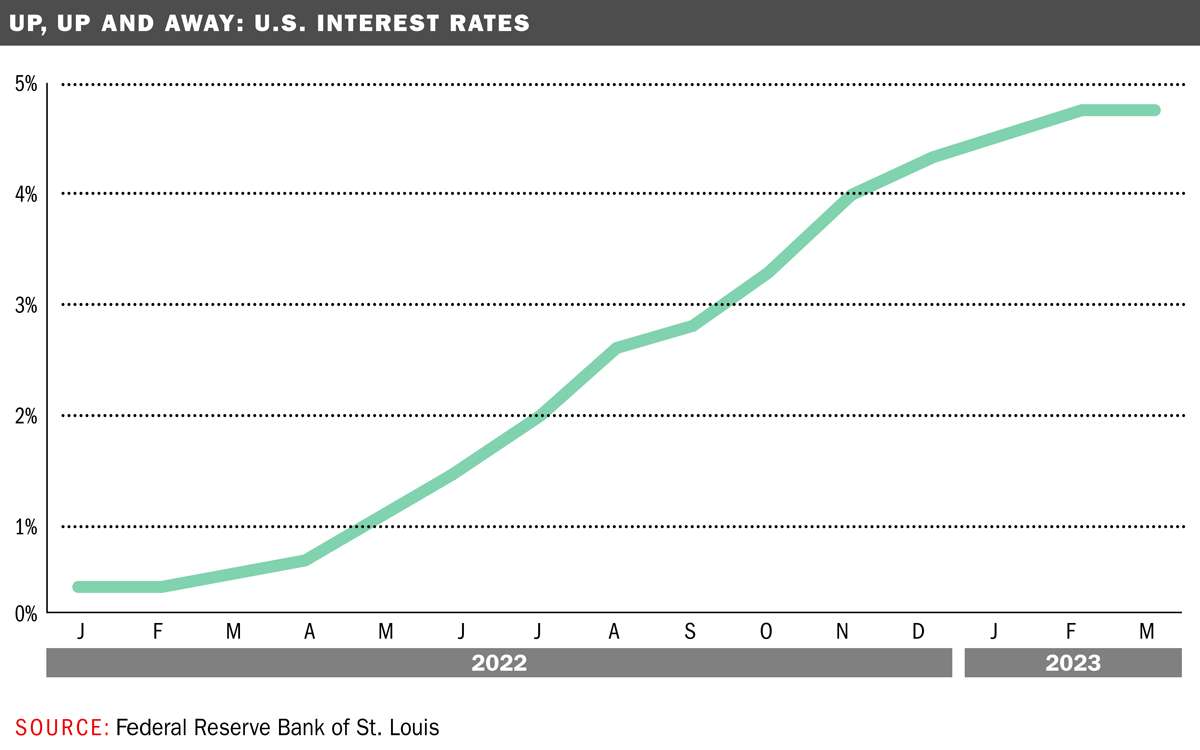

Silicon Valley Bank, a 40-year old lender that grew into the country’s 16th largest, was a prominent financier to venture capital-backed technology startups nationwide. It got into trouble by investing funds in long-term bonds when interest rates were near zero, then had to raise capital in a hurry when steeply rising rates — the Fed has hiked borrowing costs nine times over the past year, most recently by 25 basis points on March 22 — eroded the value of its investments.

The crisis hit close to home for entrepreneurs including Noah King, a Weston, Mass.-based alumnus of the Roux Techstars accelerator program in Portland who opened an account with SVB in July 2020 as he prepared to launch Popsixle, a data processing startup.

After hearing about SVB’s straits from a startup-founder text thread and on Twitter, he was able to transfer 99% of his company’s deposits to a new account at TD Bank. He has no regrets about banking with SVB, whose bankers he says were generous and committed to Popsixle’s success.

“They knew the ins and outs of startups, and it felt great to work with a partner who understood our needs.” His advice to fellow entrepreneurs: Work with a well-established bank, “but also find a banking partner who will give you personal attention.”

For SVB, the combination of a heavily concentrated depositor base, more than 90% of deposits above the $250,000 limit covered by the Federal Deposit Insurance Co. and errant risk management made for a toxic mix that sealed its doom. It was the first FDIC-insured bank to fail in two years.

Photo / Tim Greenway

Andrea Shaw, a lawyer with virtual law firm Practus LLP, boils down Silicon Valley’s missteps as an “asset-liability mismatch.”

“SVB had a plan to raise additional capital that may have worked but for the run on the bank,” says Andrea Shaw, a Portland-based partner with Practus LLP, who boils down SVB’s troubles to an “asset-liability mismatch.” She notes that accounting practices have become stronger since both the S&L and 2008 crises, “which hopefully means that this is not the start of another financial crisis.”

Rising interest rates are, in fact, a headache for all banks, says Kennebec Savings Bank CEO Andrew Silsby.

“The Federal Reserve is trying to tame inflation and has jammed short-term rates up faster than they have in over 43 years of rate policy,” he says. “That action is putting a strain on nearly all banks.” On top of that, deposits are going down across the banking sector, giving banks less capital to manage through times of trouble, he says.

“With the Fed poised to continue raising rates, we will see an increased liquidity crunch in the banking sector, as deposits tend to get scarce at this point in the economic cycle,” he says. “Banks are all fighting over deposits, which is helping the deposit customer’s interest rates that have been very low for a long time, but for banks it’s more about maintaining deposit balances to keep the delicate balance that relies on trust, faith and stability in the system.”

Keeping their distance

Seeking to distance themselves from the SVB debacle and ensuing bank failures, Maine banks wasted no time issuing public statements seeking to reassure depositors their money is safe.

“We’re here for you — and have been since 1875,” Camden National Bank said in a LinkedIn post.

“We bear no resemblance to the troubled banks in the news,” Maine Community Bank posted.

“We remain healthy, well-capitalized, diversified and prepared to support your ongoing needs,” Machias Savings Bank, told its LinkedIn followers. CEO Larry Barker commented, “Relax Mom, your money is safe.”

Spooked investors selling shares in bank stocks nationwide are the opposite of relaxed, pushing the KRE index that charts the stock market performance of smaller regional banks across the United States down 30% between Feb. 22 and March 22. (See chart.) That compares to a 1.5% drop in the broader S&P 500 Index over the same period. While declines were less steep for the handful of Maine’s publicly traded banks, three of them experienced drops in the double digits. Decliners include Camden National Bank, whose shares fell 11%.

Camden National CEO Gregory A. Dufour says that his institution maintains its credit quality in several ways, including prudent risk management when starting loan talks with a borrower.

He also says the bank works carefully with regulators, auditors and third-party teams “to ensure we have the most robust risk practices and governance standards,” adding: “Our strong credit quality, diversified customer base and strong capital are all contributors to our strength.”

At Bangor Savings Bank, Maine’s largest in terms of assets as of June 3, 2022, CEO Bob Montgomery-Rice says that only 15% of deposits are above the FDIC’s $250,000 insurance cap — well below the 40% industry average.

Photo / Courtesy of Bangor Savings Bank

Bangor Savings Bank CEO Bob Montgomery-Rice

“This is a considerably lower risk exposure, which is actively managed and safeguarded,” he says. He’s not worried about flattening deposit growth in 2023 amid increased consumer spending and investments by businesses, he says. “Through the priority of safeguarding customer deposits and our diversified deposit base, we are in a strong position.”

At Machias Savings, Barker says his CFO knows of only one customer who has moved funds out of the bank in reaction to the current turmoil, and says that his bank’s loans, deposits and balance sheets are well-diversified.

“I can say with confidence the same thing I said over and over during the pandemic: Community banking never looked so good,” he says.

Trade groups weigh in

Despite bank woes in other parts of the country, neither the Maine Bankers Association nor the Maine Credit Union League perceive any red flags for the state’s financial sector.

Maine Credit Union League President and CEO Todd Mason says that while the bank closures in California and New York are “troubling,” they haven’t sounded any alarms over liquidity at Maine institutions.

“A fundamental tenet of running a healthy financial institution is diversification,” he says. “That is exactly what our credit unions do, and exactly what SVB and Signature did not do.” For small businesses or entrepreneurs who belong to credit unions, Mason says he would tell them that those institutions are the safest place to keep their money.

Looking ahead, Mason says that Maine credit unions will continue to invest heavily in compliance and risk management to avoid the “fatal flaw” that SVB and Signature made of having heavy concentrations, be that in types of deposits, loans or investments. “As an additional check beyond the internal and third-party audits credit unions do, regulators also regularly review for concentration risk, among other areas, to further help ensure the safety and soundness of the Maine financial service industry.”

Mason also notes that in contrast to banks, credit unions are not-for-profit entities.

“Members place their trust in credit unions to safeguard their assets and secure their financial futures,” he says. “Carrying out this responsibility is our top priority.”

Along similar lines at the Maine Bankers Association, President and CEO Jim Roche underscores that Maine banks are well-run and without heavy concentrations of tech or crypto currency startups like Silicon Valley Bank and Signature Bank had.

“Most Maine banks are community banks providing residential mortgages, small business loans and lines of credit, and savings and deposit services for working men and women,” he says. He also notes that most Maine bank accounts fall under the FDIC’s $250,0000 insurance cap.

Entrepreneur seeks third bank

So what about entrepreneurs with uninsured holdings and little credit history in the United States? That’s the case for Max Echeverria, the Chilean-born founder of Portland-based startup Eskuad, a mobile data platform designed for field operations. Like King, he had an account at SVB. At the advice of an investor who tipped him off to the imminent bank collapse, he moved most of the money out of his account just in time. “I hadn’t realized how stressed I had been until after the money went through,” he says.

The transfer went to an existing account at corporate payments platform Brex, while leaving a nominal amount with the new SVB bridge bank.

“It’s insured, so it’s a safe bet for now,” he says.

Echeverria, one of nine employees at Eskuad, is now looking to open a third account at a large commercial lender. A foreign national without much of a U.S. credit record, he’s hesitant to bank with any smaller institution just yet while keeping his options open as an early-stage startup.

“We don’t have many assets,” he says at the Roux Institute campus he uses as an office when he’s in town, “just cash, people and computers.”

Photo / Tim Greenway

Max Echeverria, founder of Portland-based startup Eskuad, was able to transfer most out of his money out of his Silicon Valley Bank account in the nick of time.

Mainebiz web partners

Most Recent

Most Recent

0 Comments