J.D. Power 2019 U.S. Retail Banking Satisfaction Study

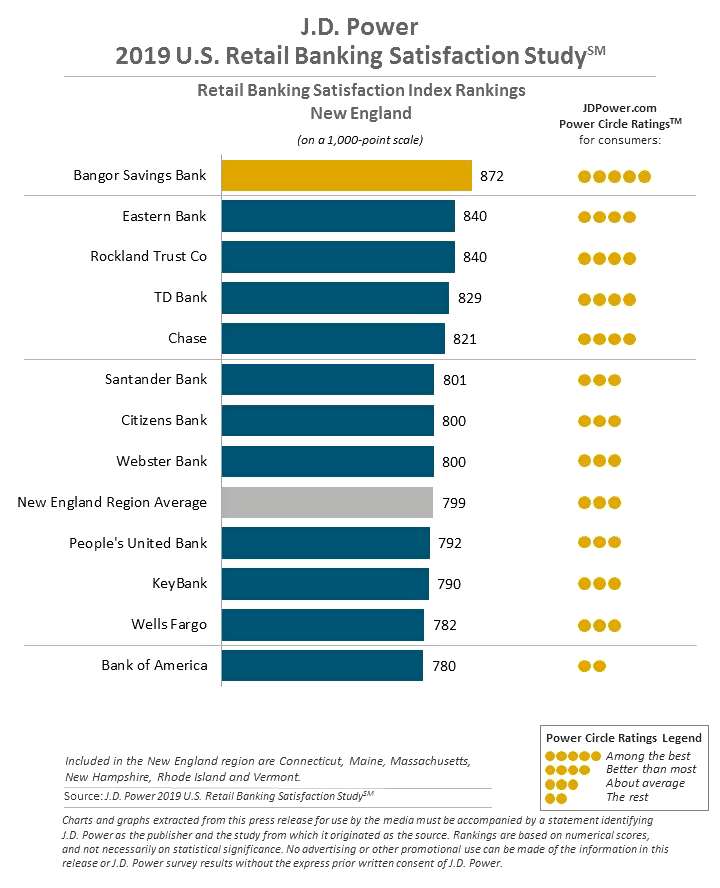

Chart shows how Bangor Savings Banks compares with other large banks in New England for customer satisfaction in the 2019 J.D. Power U.S. Retail Banking Satisfaction Study.

Please do not leave this page until complete. This can take a few moments.

For the fourth time in five years, Bangor Savings Bank has received the highest score among qualifying retail banks in the New England region in the J.D. Power 2019 Retail Banking Satisfaction Study.

The bank’s score of 872 out of a possible 1,000 points in the 2019 study earned it the highest Power Circle Rating of “among the best," and beat the New England region average score by 73 points. The bank increased its score from the previous year and remained No. 1 in the region while welcoming and integrating employees and customers gained through its 2018 acquisition of New Hampshire-based Granite Bank.

The 14th annual customer satisfaction study is the longest-running and most in-depth survey of the U.S. retail banking industry, with customers evaluating various aspects of their banking experience. The 2019 study is based on responses from more than 84,000 retail banking customers of more than 200 of the largest banks in the United States regarding their experiences with their retail bank. It was fielded in quarterly waves from April 2018 through February 2019.

“We are honored to once again be recognized by J.D. Power,” Bangor Savings Bank President and CEO Bob Montgomery-Rice said in a news release. “Our employees continue to be the driving force behind our success. Whether in person at a branch, on the phone in Bangor Support, or behind the scenes developing innovative solutions, they work hard to create incredible experiences for our customers each and every day.”

Montgomery-Rice said the bank’s “You Matter More” mission statement “continues to be more than a tagline.”

““It has been the foundation of our promise for 167 years and we are proud to support the people and places we serve,” he said.

The J.D Power study asked banking customers for objective feedback on various aspects of their banking experience, including account opening, convenience, channel activities (branch, assisted online, ATM, mobile, website, Interactive Voice Response and call center), problem resolution, communication and advice, and product offerings and fees.

Key findings and trends from the J.D. Power 2019 Retail Banking Satisfaction Study:

In the 10 years since the financial crisis, bank reputations have declined: Since 2009, overall retail bank customer satisfaction has improved, as have satisfaction scores with in-person branch service, online banking and ATMs. Also, since 2009, satisfaction with mobile banking has improved, as have customer knowledge of the features, benefits and fees structure associated with their banking products. Customers currently view their banks as being more innovative and financially stable. However, customer perceptions of retail banks having a good reputation and being customer driven are lower in 2019 than in 2009. The industry has improved convenience and driven increased levels of operating efficiency, but a trade-off for banks is a decline in easy interaction, providing advice and strengthening customer relationships.

Growth in overall customer satisfaction hampered by unresolved problems: Overall customer satisfaction with retail banks is 807 (on a 1,000-point scale), up just one point from 2018. This increase is due to an improvement in customer satisfaction with products and fees, but declining satisfaction in the areas of problem resolution and telephone customer service offset the gain. Telephone is the most frequent servicing channel customers use to resolve problems. Customer satisfaction scores also decline in online assisted customer service (online chat, email or social media channels). Of all the delivery channels measured in the study, only ATM increases in customer satisfaction.

Problem resolution is a lingering banking pain point: The 2019 decline in customer satisfaction with retail bank problem resolution and the timeliness of banks in solving problems are reminders that failing to execute on the basics have negative effects on reputation. Customers have long memories and their brand image ratings for bank reputation decline dramatically when they experience problems. Reputation declines further when customers perceive that problems are unresolved or resolved in a manner put the bank’s interests ahead of theirs.

Big banks gird for battle for digital customers with midsize and regional banks: The Big 62 banks have benefited from improved customer satisfaction among customers under age 40 in recent years and, in 2019, attain higher satisfaction scores than regional and midsize banks. This demographic gives the Big 6 banks the highest scores for convenience; ATMs; mobile and online banking; innovation; and financial advice. However, the smaller banks recognize the strategic importance of remaining competitive in digital. Across all age groups included in the study, overall satisfaction increases more notably among digital-centric customers of midsize and regional banks than among customers of Big 6 banks.

Bangor Savings Bank, with more than $4 billion in assets, offers retail banking to consumers as well as comprehensive commercial, corporate, payroll administration, merchant services, and small business banking services to businesses. The bank, founded in 1852, is in its 167th year with 58 branches in Maine and New Hampshire and on the web at www.bangor.com. The Bangor Savings Bank Foundation was created in 1997. Together the bank and its foundation invested more than $2 million into the community in the form of nonprofit sponsorships, grants and partnership initiatives last year. Bangor Savings Bank is an equal opportunity employer.

The Giving Guide helps nonprofits have the opportunity to showcase and differentiate their organizations so that businesses better understand how they can contribute to a nonprofit’s mission and work.

Learn More

Work for ME is a workforce development tool to help Maine’s employers target Maine’s emerging workforce. Work for ME highlights each industry, its impact on Maine’s economy, the jobs available to entry-level workers, the training and education needed to get a career started.

Learn More

Whether you’re a developer, financer, architect, or industry enthusiast, Groundbreaking Maine is crafted to be your go-to source for valuable insights in Maine’s real estate and construction community.

Learn moreThe Giving Guide helps nonprofits have the opportunity to showcase and differentiate their organizations so that businesses better understand how they can contribute to a nonprofit’s mission and work.

Work for ME is a workforce development tool to help Maine’s employers target Maine’s emerging workforce. Work for ME highlights each industry, its impact on Maine’s economy, the jobs available to entry-level workers, the training and education needed to get a career started.

Whether you’re a developer, financer, architect, or industry enthusiast, Groundbreaking Maine is crafted to be your go-to source for valuable insights in Maine’s real estate and construction community.

In order to use this feature, we need some information from you. You can also login or register for a free account.

By clicking submit you are agreeing to our cookie usage and Privacy Policy

Already have an account? Login

Already have an account? Login

Want to create an account? Register

In order to use this feature, we need some information from you. You can also login or register for a free account.

By clicking submit you are agreeing to our cookie usage and Privacy Policy

Already have an account? Login

Already have an account? Login

Want to create an account? Register

This website uses cookies to ensure you get the best experience on our website. Our privacy policy

To ensure the best experience on our website, articles cannot be read without allowing cookies. Please allow cookies to continue reading. Our privacy policy

0 Comments